Bitcoin is Falling Behind

Not just because of the price decline

Like gold or diamonds, bitcoins can be exchanged for dollars and euros because people agree that they’re worth the market price. Bitcoins aren’t a good or service, they don’t produce cash flow like rent or interest and they’re not a claim on assets like oil, real estate or stocks. Mostly, there is just the broad social consensus that bitcoins are valuable.

And so they are.

Lots of things shape this social consensus: Narratives about use cases and bitcoin’s properties (only 21M coins! Inflation hedge!); evidence that bitcoin is being ‘adopted’ (El Salvador!); get rich quick stories, fear of missing out, the cult following, and more.

Bitcoin faces real headwinds, but all you ever hear from its loudest proponents is the same vapid cheerleading. In case you needed it, here is a summary of where things stand. Bitcoin might have rallied 5% today, but as a tool, a culture and an asset, it’s not doing great.

Not Inflation Hedge

Bitcoin is meant to hedge holders against inflation, but it simply doesn’t. While US inflation climbed from 2% in early last year to 9% this summer, bitcoin fell from $68k to $20k. Whenever monthly CPI data came in hotter than expected, bitcoin regularly tanked a few percent on the news, as Joe Weisenthal and Tracy Alloway reminded us on their podcast.

Bitcoin investors are -50% year to date and -53% in purchasing power terms as inflation has climbed to the highest level in 40 years. So much for the ‘hard money’ inflation hedge.

Too Volatile

Bitcoin’s volatility is supposed to fall as ‘adoption’ increases, but it’s been a decade and it hasn’t. As I’ve written before, short-run volatility is enormous and isn’t trending down (red line) and price movements over the long term are colossal (black line, note the log scale on the y-axis).

As long as bitcoin has these properties, it can’t fulfill its original purpose of being a currency. That’s part of the reason why El Salvador’s ‘adoption’ has been such a flop and why Salvadorans aren’t using bitcoin for much at all.

None of this rules bitcoin out as a long-run store of value that can complement an investment portfolio with strong expected returns that are uncorrelated from other investments. Except that bitcoin —>

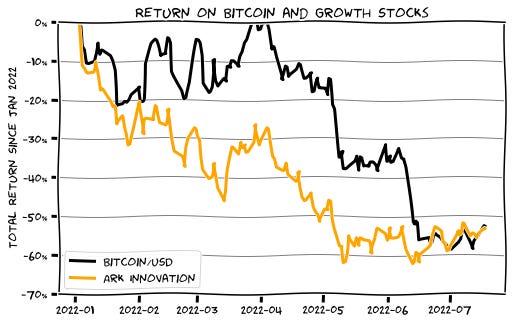

(Sort of) Trades Like Growth Stocks

Here’s a chart of the total returns on bitcoin and a Cathy Wood’s Ark Innovation ETF (a basket of speculative growth stocks like Zoom, Tesla, etc) for a position opened this January.

Both positions are down about 55% year to date and move broadly in tandem, suggesting they provide exposure to similar things. Of course, correlations hold until they don’t and bitcoin could decouple from speculative growth stocks (up or down) in the future. But for the past six months, bitcoin hasn't given investors the uncorrelated market-beating returns they were sold.

Returns

Speaking of which, bitcoin is also getting less attractive to traders that want to make money and don’t care about the ‘culture’ or ‘technology.’ Annualized returns from high to high (in red) or low to low (in blue) have consistently decreased over market cycles.

People that bought the top in 2018 and sold the top this year only made a 37% yearly return. That’s very high, but it's a far cry from the 307% return between 2011 and 2014. Of course, returns could accelerate and past performance is not indicative of future results. But returns sure have slowed!

Privacy

We were told that Bitcoin is anonymous and private, which is meant to be good, but that’s not very true either. Governments are getting better at linking wallet addresses on the blockchain (hexadecimal codes like bc1qxy24…) with the real world firms and individuals that own them.

Take what happened in Canada as an example. Early this year, truckers protested against vaccine mandates and held up traffic at the border for weeks. Trudeau’s government froze their bank accounts to get them to stop and sympathizers sent them bitcoin donations to bypass the restrictions.

It didn’t go as planned. Six of the 21 bitcoins were seized. Bitcoin turned out to be relatively easy to surveil, shut down, and deplatform by a determined state. For actual anonymity and privacy, there are ‘privacy coins’ like Monero.

Culture

Bitcoin culture is alienating and unsavory. I hate to name names, but take the CEO of Microstrategy, a public US company that bought $4B of bitcoin and is down about $1B on the position. Look at this nuance:

Or the president of El Salvador, who claims to day trade bitcoin from the bathroom while naked, presumably with taxpayer money. Or the armies of anonymous trolls that tell skeptics to ‘have fun staying poor’ or the crypto influencers:

And then, whenever a thoughtful bitcoin proponent like Nic Carter breaks the party line and endorses another blockchain, they are publicly crucified. Who would want to be associated with this laser-eyes crowd? It’s embarassing.

Sacred Truths

Many of the remaining myths about bitcoin have been busted this cycle. Notably, bitcoiners used to say that each cycle’s peak is always lower than the next cycle’s bottom. Well, that proved to be false. The stock-to-flow price prediction model was also debunked.

Stablecoins

Bitcoiners like to believe that USD-linked stablecoins and bitcoin are complements, mostly because Tether (allegedly) uses its USD reserves to buy bitcoin on the open market and pump the price. I’d argue this is wrong though.

Bitcoin and fully-backed stablecoins are more like substitutes, at least in emerging markets. As stablecoins ballooned from five to $150 billion over the past two years, markets for USDT against local currencies like the Venezuelan Bolivar and Turkish Lira became increasingly deep and liquid.

In these countries, now that bitcoin and stablecoins are both broadly available, people prefer holding synthetic dollars over volatile bitcoin, cannibalizing demand.

Ethereum

Bitcoin is still the largest crypto asset by market capitalization, but on lots of other metrics, it's lagging far behind competitors.

These days, most of the crypto wallets and applications that people actually doownload and use (like NFTs and DeFi) are on Ethereum. Most of the startups that got funded this cycle are on Ethereum. And the majority of crypto developers work on Ethereum. Sure, much of the activity, products and companies are speculative or Ponzi-adjacent, but at least people are using the blockchain and paying fees to do so!

Banks

Bitcoins and other crypto assets just sit on blockchains without earning interest, but people like earning interest, so a bunch of crypto ‘banks’ popped up in the past two years to offer crypto interest. They started taking ‘deposits’ in bitcoin and other coins to ‘put them to work’ and pay out returns to ‘depositors’ as interest after taking a cut.

There was no regulatory oversight and a bunch of these ‘banks’ like Celsius Network and Voyager went bankrupt. It turns out that they didn’t do risk management or were outright Ponzis. It also turned out that ‘deposits’ weren’t deposits; they were uninsured unsecured loans.

Predictably, a bunch of people are going to lose their shirts. It’s mostly regulators’ fault for letting it happen, but it’s still not a good look for bitcoin.

The Respectable Thesis

The most (and only?) reasonable case for Bitcoin isn’t all this mumbo jumbo about cyber hornets, hyperbitcoinization, the ‘halving thesis’, and ‘nation state adoption,’ etc.

It’s three sentences long:

Bitcoin aspires to be a digital reserve asset and store of value but with (arguably) better properties than gold. It uses an enormous amount of energy, but it can be self-custodied and is easier to buy, sell, and move across borders than gold. It’s easy to audit and doesn’t require central intermediaries.

You can disagree with this value proposition, but at least there’s a clear idea there.

Bitcoin to Zero?

Thing aren’t going great, but no.

We’re well past the point where the consensus that sustains bitcoin’s value can just collapse. Bitcoin could underperform other assets or trade sideways or down for a long time, perhaps forever. But despite the zealots, their cringey boosterism and own-goals, bitcoin almost certainly isn’t going away.

(If you have questions or comments, reply to this email or comment at the bottom of the web version. I reply to everything! Also, press the like button if you liked the post! Thanks for reading!)