El Salvador Completes Debt Buyback

Saving the country 1% GDP. But what's the catch?

As little as two months ago, Wall Street thought El Salvador had a 50% chance of defaulting on the $800M sovereign bond due January 2023. With a gaping fiscal deficit, YOLO Bitcoin buys from the president and no IMF deal in sight, the 2023 bond traded as low as 65 cents on the dollar this summer — a colossal discount for debt maturing in just a few months.

But then, to the surprise of many, President Bukele offered to repurchase the 2023 bonds and the 2025 bonds at their deeply discounted market prices. The offer signaled that his government plans to keep paying the sovereign debt and caused the implied default probability for January to more-than-halve to 20%.

Well, the operation is complete now. El Salvador bought back its own bonds, saving taxpayers about 1% of GDP in future debt payments. For reference, one percent of GDP in the US is 200 billion dollars. So it’s a lot. But let’s be real. The operation’s success doesn’t change the fact that El Salvador needs to cut spending or raise taxes (or both) to avoid defaulting on the country’s debt beyond the presidential elections set for 2024.

Savings for Taxpayers

El Salvador spent $360M to repurchase $133M in notional value of the 2023 bond at 91 cents1 and $433M of the 2025 bond at 54 cents2. As a result, the country wiped out $206M in net debt. Plus, by retiring the bonds from investors before they mature, El Salvador saved $69M in future interest expenses.

All in all, the operation will net the country $274M over two years and four months. For a $360M repurchase ‘investment’ today, the country gets $634M in ‘payoffs’ over 28 months, as the chart below shows:

Is this a good deal? One way to tell is by looking at its internal rate of return (IRR), which comes out to 40%. A 40% nominal rate of return is a very (extremely) high number. If Bukele’s plan is to continue paying the sovereign debt, and the market wants to keep selling El Salvador’s bonds at deep discounts, then he should probably keep buying it. In fact, that is exactly what he announced. El Salvador is now apparently launching a second debt repurchase:

Saving taxpayer money with debt repurchases is great. But it only makes sense if the country is not going to default in the medium run. If the country is going to default sometime soon, say after the elections in 2024, then the best option is to hoard USD, not hand precious dollars over to creditors.

If the country is going to default, the best option is to keep the power dry, maintain solid USD reserves and save them for socially important things (like pensions and schools and hospitals), not spend them paying external creditors, who are going to have their debt restructured after the default anyways.

So how can El Salvador —>

Avoid Sovereign Default?

The answer is easy to write down and difficult to do: by cutting government spending or raising taxes or both. This is euphemistically called ‘fiscal adjustment’ or ‘fiscal consolidation.’ But basically it just means balancing the budget. Obviously, this is never popular. People don't like being taxed and often their livelihoods depend on government services and benefits.

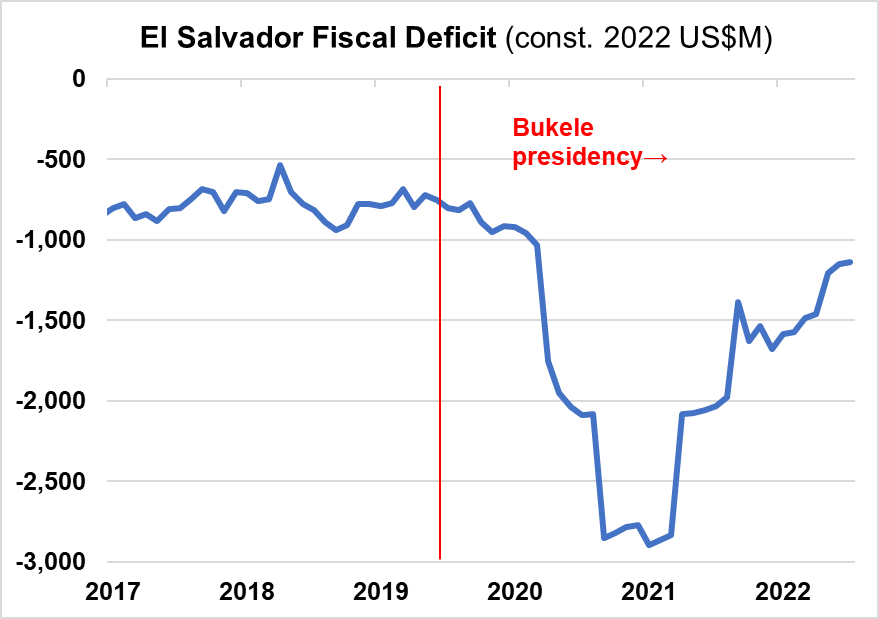

Here’s the country’s deficit:

It exploded with COVID, like in every other country. Then it narrowed sharply in 2021, but not to 2017-2019 levels.

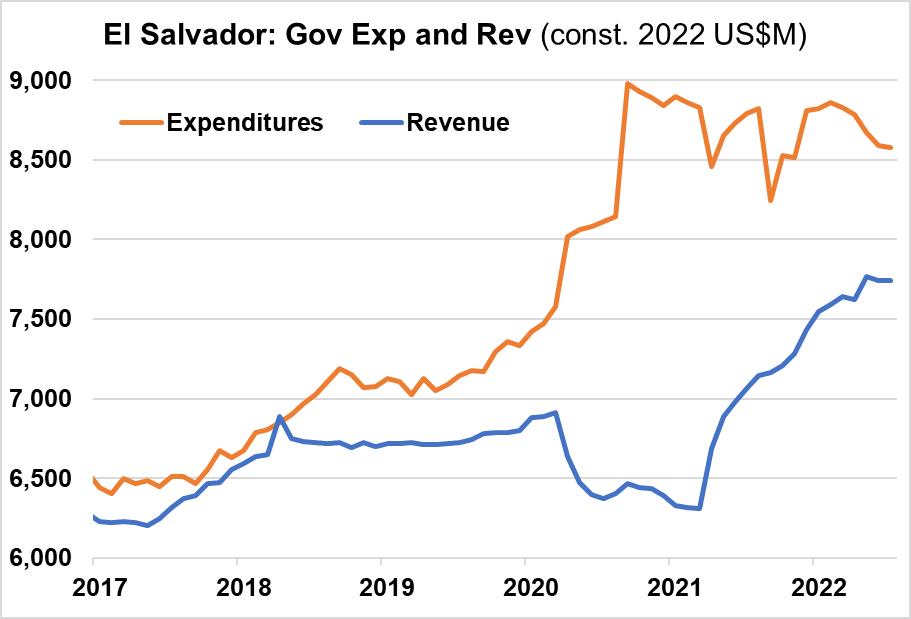

Concerningly, a lot of the deficit reduction has come from strong growth in tax revenues driven by inflation and the economic recovery. Government spending is actually still at ‘emergency’ levels, even though the health emergency is over:

The crazy high expenditures in orange were initially hospitals and vaccines and cash transfers to people in lockdown, etc. Fair. But now they’re regressive gasoline subsidies and other ad-hoc spending that’s a bad use of public money. It needs to stop for El Salvador’s finances to be sustainable again.

If the country keeps running a billion dollar plus fiscal deficit, it will run out of cash within a few years and will be faced with the impossible choice of paying Wall Street or paying local pensioners and teachers and firemen and nurses. Obviously, if forced to chose, Bukele will favor domestic voters and default on foreign bondholders, as the majority of countries in deep financial distress do.

To avoid having to make that choice, El Salvador needs to balance the budget. And the success of the debt buyback doesn’t change this simple fact.

Timelines, Budgets and Elections

This is El Salvador’s payment schedule on the foreign bonds after the repurchase:

There’s still a big payment this January (though its smaller now) and there’s a spike in 2025 (though its much smaller now — about half as big as before). Of course, there’s also all the domestic debt, which is mostly held by domestic banks and pension funds and is relatively easy to roll over. And there’s the multilateral debt to the World Bank and IDB and so on.

With the buyback, the payment schedule has gotten easier and El Salvador’s bond prices have risen somewhat to reflect that. But in my opinion, Wall Street is still overestimating the likelihood of default in the medium run, as they did for the past year with the January 2023 bond.

El Salvador will prepare the budget for 2023 in a few months for the presidential campaign next year ahead of the elections in early 2024. On one hand, Bukele will want to keep the economy juiced up with stimulus and subsidies to keep people happy and win the election. On the other hand, presumably, his government will want to reduce non-essential spending to narrow the deficit and avoid defaulting on policemen or some other important domestic stakeholder to keep paying the debt.

We don’t know how those forces will balance out, though. If El Salvador budgets a huge deficit for 2023, that will accelerate the timeline for expected default. If the country budgets a big spending cut for 2023, that will delay default.

The Road Ahead

With 84% popularity, Bukele can probably afford to cool spending. Fiscal adjustments are politically costly, but El Salvador’s president has political capital to spare, at least for now. A deal with the IMF to make that adjustment smoother should also be possible. Bitcoin adoption has been a flop and the government knows it so it shouldn’t be too hard to make some bitcoin concessions to the IMF to get a deal.

The million dollar question right now is not whether Bukele can carry out a fiscal adjustment. Clearly, he can. The million dollar question is whether he wants to. Next year’s budget will be prepared this November and December, so we’ll find out soon enough.

BONUS: El Salvador Podcast

I was on the Crypto Critics’ Corner podcast recently talking about El Salvador, sovereign default, bitcoin, the volcano bond and more. It was a blast. Hosts Cas Piancey and Bennett Tomlin do gods work by keeping tabs on all the craziness in crypto. If you have the time, have a listen! (Also on Spotify, Apple podcasts, and other platforms).

For $123M cash plus accrued interest

For $237M cash plus accrued interest

I wonder how the sovereign debt market would respond to bukele's illegal reelection given that if he breaks salvadoran law to be reelected possibly indefinitely, how would investors have guarantee that his government will honor future debt payments? It seems to me that the salvadoran government has budgeted everything to ensure short term conditions because their sole goal appears to be to remain in power, but that there is no plan for the mid to long terms. Is a run on the banks still a likely scenario in the months right after reelection? I learned from a previous post that you are venezuelan, so I've wondered if you are aware or even know personally the venezuelan members of bukele's staff such as Sarah Hanna Georges, Lorenzo Rey, Lester Toledo, Miguel Sabal, Miguel Arevalo, Tomas Hernandez, Roddy Rodriguez, Juan Carlos Gutierrez, Santiago Rosas, Ernesto Herrera, etc. all of whom advice bukele on finance, government economic policy, bitcoin, etc. There is also parallelisms between Hugo Chavez and nayib bukele in terms of populist, demagogue leaders who dismantle democratic institutions to amass and remain in power while pushing their countries to economic catastrophe; with that said I would like to know if you can illustrate what that means for the salvadoran economy drawing from venezuela's recent economic history and granted the vast and diverse differences between el salvador and venezuela?